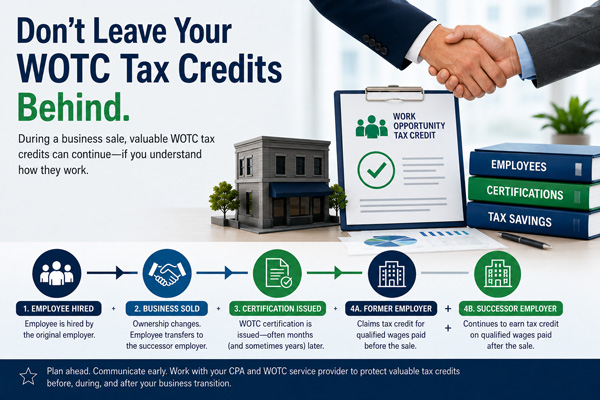

Selling a business can create unexpected WOTC tax credit issues and opportunities long after the transaction closes. Because employee certifications may not be issued until months (or even years) later, both sellers and successor employers should understand how delayed certifications can affect their tax credits.

When business owners prepare to sell their company, they naturally focus on things like purchase agreements, employee transitions, customer relationships, and tax planning. An item that is often overlooked is the status of pending Work Opportunity Tax Credit (WOTC) applications.

Because WOTC certification frequently takes months, and in some states several years, valuable tax credits may still be working their way through the certification process after ownership has changed.

Without careful planning, those tax credits can be misunderstood, overlooked, or claimed incorrectly.

Tax Credits Earned Before the Sale May Still Belong to the Original Employer

Generally speaking, WOTC tax credits attributable to qualified wages paid by the original employer remain available to that employer, even if an employee’s WOTC certification is not issued until after the business has been sold. This is an important consideration because, in some states, the WOTC certification process for individual employees may take anywhere from a few weeks to multiple years.

This can create an unusual situation:

- The certification arrives after the business has been sold.

- The former owner may no longer be actively involved in the business.

- Accounting records may have been archived.

- The individuals responsible for the transaction may assume the opportunity has passed.

In many cases, however, that opportunity has not passed.

Depending on the circumstances, those certifications may support amended tax returns or other tax benefits relating to the period before the acquisition. Your CPA should determine the appropriate tax treatment, while your WOTC service provider can help identify which certifications and wages relate to the pre-acquisition period.

Successor Employers May Continue Receiving WOTC Benefits

Business owners are often surprised to learn that, generally speaking, a successor employer steps into the shoes of the previous employer for WOTC purposes. Employees who were hired and certified by the original employer before the acquisition may continue generating WOTC tax credits for the acquiring employer, subject to the normal WOTC limitations and maximum credit amounts.

This does not transfer tax credits attributable to wages paid before the acquisition. Rather, it allows the successor employer to continue earning WOTC tax credits on its own qualified wages paid after acquiring the business.

Transferred Employees Are Not New Hires

Another common misunderstanding occurs after an acquisition when employees become part of the acquiring company. Generally speaking, the IRS does not treat these transferred employees as new hires for WOTC purposes.

As a result:

- Employees transferred from the previous employer cannot be screened again for WOTC eligibility simply because ownership changed.

- If an employee was previously certified, the acquiring employer generally continues under that existing certification rather than obtaining a new one.

- If an employee was not WOTC eligible at the time they were originally hired, the acquiring employer generally cannot create a new WOTC opportunity simply because ownership changed.

Understanding this distinction can prevent unnecessary screening efforts and avoid compliance mistakes.

Communication Is Essential During a Business Transition

Whenever a business is being sold, both the seller and purchaser should discuss any pending WOTC activity with their tax advisors and WOTC service provider.

Questions worth addressing include:

- How many WOTC applications are still awaiting certification?

- Which certifications may still produce tax credits for the selling employer?

- Which employees may continue generating WOTC benefits for the acquiring employer?

- How should future certifications be tracked after the transaction closes?

Addressing these questions early can help ensure that valuable tax credits are properly identified, documented, and claimed by the appropriate employer.

If a business acquisition is anticipated, now is the time to review all pending WOTC applications with your CPA and WOTC service provider. Doing so can help ensure that certifications issued months (or even years) after closing are properly tracked and that the resulting tax credits are claimed by the appropriate employer.

Every acquisition is unique, and WOTC treatment depends on the specific facts of the transaction. Business owners should work closely with their CPA and experienced WOTC professionals to ensure these opportunities are not overlooked during the transition.

WOTC Planet does not provide tax, accounting, or legal advice. This content is for informational purposes only.

One response