WOTC’s 2026 reauthorization cycle and current legislative pause naturally raise an important question for employers:

Should we continue screening new hires for WOTC while Congress is navigating the program’s reauthorization cycle?

When a tax credit’s legislation enters a reauthorization cycle, it’s reasonable to pause and evaluate. This article provides context based on the program’s long history and how WOTC has been administered during past reauthorization cycles.

While only Congress can authorize or reauthorize the program, the consistent best practice (based on decades of precedent and agency guidance) is to continue screening and submitting applications. Continue reading to understand why.

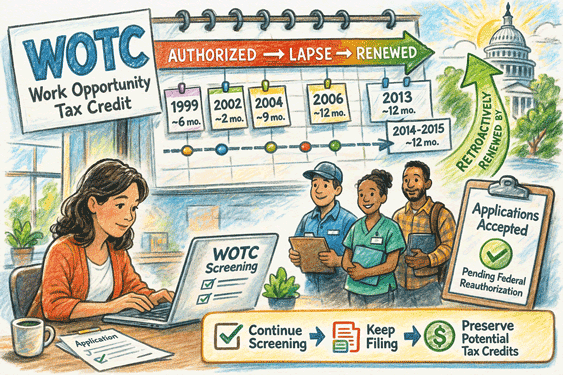

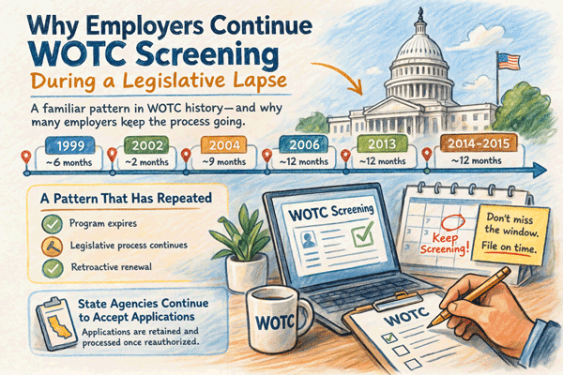

A Pattern That Has Repeated Over Decades

During its 30-year history, the Work Opportunity Tax Credit (WOTC) has been renewed thirteen times as part of the federal “tax extenders” process. In more than half of those occasions, Congress allowed the program to enter a temporary hiatus while new legislation was being crafted and approved. Every time, the pause was followed by a full retroactive reinstatement.

In other words, Congress reauthorized WOTC, and patient employers (who continued screening new hires and filing their applications) were rewarded with the full tax credit amount.

From a legislative standpoint, the current reauthorization cycle follows a familiar pattern.

What Happened During Previous Cycles?

During prior reauthorization cycles, the U.S. Department of Labor instructed State Workforce Agencies (SWAs) to continue receiving WOTC applications within the required filing timeframes. Employers were expected to continue timely screening. While certifications could not be issued until reauthorization legislation was approved, state agencies continued to receive applications and then issued the certifications after Congress acted.

State agencies are communicating similar expectations today. For example, the California Employment Development Department’s WOTC web page currently states:

Employers should continue submitting WOTC applications within [the] required timeframes. Applications with start dates of January 1, 2026, and after will be accepted and retained pending federal reauthorization.

See EDD CA WOTC

What Does This Mean to Employers Today?

Historically, employers who continued screening and submitting applications during reauthorization cycles were positioned to receive tax credits once the program was reinstated. By contrast, if screening is paused, WOTC-eligibility information is not collected, and applications can not be filed. When the program is later reauthorized, most, if not all, of the potential credits can be lost.

While only Congress can authorize or reauthorize the program, the consistent best practice (based on decades of precedent and agency guidance) is to continue screening and submitting WOTC applications.

For more information, Work Opportunity Tax Credit (WOTC) Reauthorization Update: What Employers Should Know.

WOTC Planet does not provide tax, accounting, or legal advice. This content is for informational purposes only. Employers should consult their tax and legal advisors when evaluating changes to HR or PII handling policies.

One response